Hey there! Let’s dive into a topic that might feel a bit daunting: getting denied for a mortgage. If this has happened to you, take a deep breath and know you’re not alone.

Many homebuyers face this challenge, but the great news is that a denial doesn’t mean the door to homeownership is closed forever. It’s just a detour. Let’s chat about why it happens, what you can do to turn things around, and how to make your next attempt a success.

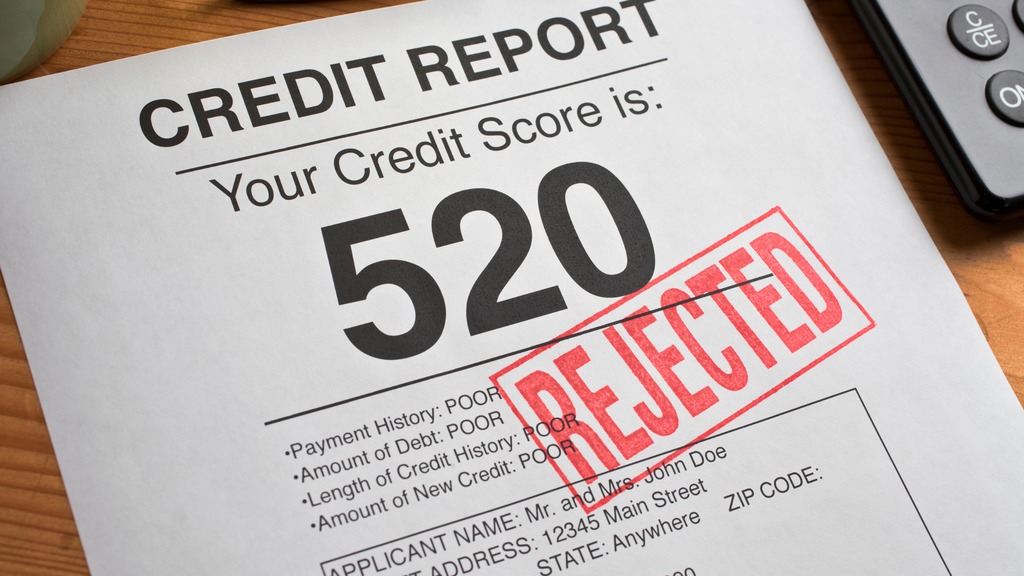

Why Was Your Mortgage Denied?

Understanding the why behind a denial is key. Here are some of the most common reasons lenders might say no:

Low Credit Score: Your credit score gives lenders insight into your financial habits. A low score can raise red flags.

Insufficient Income: If your income doesn’t match the loan amount you’re requesting, it could be a problem.

High Debt-to-Income (DTI) Ratio: Lenders like to see that your monthly debts don’t take up too much of your income

Employment Concerns: Recent job changes or gaps in your employment history can make lenders uneasy.

Missing Paperwork: A lack of proper documentation can stall the process.

Low Appraisal Value: If the home’s appraised value is less than the sale price, it complicates the loan.

What Should You Do After a Mortgage Denial?

Don’t let a denial discourage you! Here’s how to bounce back stronger:

Understand the Reason for Denial: Lenders are required to provide an explanation. Use this as a roadmap for improvement

Check Your Credit Report: Review it for errors or areas to improve, like paying down outstanding balances.

Pay Down Debt: Reducing your DTI ratio can boost your application’s appeal.

Save for a Larger Down Payment: A bigger down payment shows lenders you’re serious and reduces the loan-to-value ratio.

Work with a Mortgage Broker: They can connect you with lenders who specialize in your financial situation.

Explore Different Loan Options:

FHA Loans: Great for those with lower credit scores.

VA Loans: Perfect for veterans and active-duty service members.

USDA Loans: Ideal for buyers in rural areas.

Will You Get Approved If You Try Again?

Absolutely! Many buyers who are initially denied end up securing a mortgage later. Here’s how to increase your chances:

Give Yourself Time: Use the time after a denial to improve your finances and address the lender’s concerns.

Get Pre-Approved: A pre-approval can help you understand your budget and show sellers you’re serious.

Consider a Co-Signer: A trusted co-signer can help strengthen your application.

Shop Around: Every lender has different criteria. One lender’s “no” could be another’s “yes.”

Ready to Try Again?

A mortgage denial is just a stepping stone on your journey to homeownership. With the right steps and guidance, you can overcome this obstacle and achieve your dream of owning a home. If you have questions or need help navigating your next steps, let’s chat! We’re here to guide you every step of the way.